Are your financial statements truly audit-ready, or just “audit-prepared”?

The question above is not theoretical. It is the standard that auditors apply in practice. Across engagements, the gap between “prepared” and “audit-ready” becomes immediately visible.

Finance teams that appear organized internally often struggle to produce consistent audit evidence under external scrutiny. Requests escalate, reconciliations are revisited, and documentation is reconstructed under time pressure.

From an audit standpoint, this is not a timing issue. It is a breakdown of how financial statements are built. Audit-ready financial statements are not a year-end output. They are the result of a controlled financial reporting environment in which accuracy, traceability, and documentation are embedded in daily operations.

Key Takeaways

- Audit delays are most commonly driven by poor documentation and inconsistent reconciliations.

- Structured close processes and pre-prepared schedules lead to fewer audit adjustments.

- Continuous audit readiness improves efficiency and reduces disruption.

- Strong internal controls directly reduce audit scope and testing requirements.

- Well-supported accounting estimates are critical in avoiding audit slowdowns.

Audit Readiness Is a Reflection of Process Discipline

Audit outcomes are shaped less by technical accounting knowledge and more by execution discipline. One of the most common causes of audit delays is

incomplete or poorly organized financial records, particularly when reconciliations and supporting schedules are not maintained consistently throughout the year.

This aligns with what auditors encounter in practice. When documentation is fragmented, audit procedures expand, timelines extend, and costs increase. Similarly, organizations with structured close processes and pre-prepared audit schedules experience significantly fewer audit adjustments and smoother fieldwork execution.

Inefficient preparation does not just create friction. It consistently leads to extended audit timelines, as auditors are forced to perform additional procedures, request missing documentation, and re-test unsupported balances. From a risk perspective, this matters because the objective of an audit is to identify

material misstatements.

When processes lack discipline, the likelihood of misstatement increases, and auditors respond by increasing the depth and scope of their procedures.

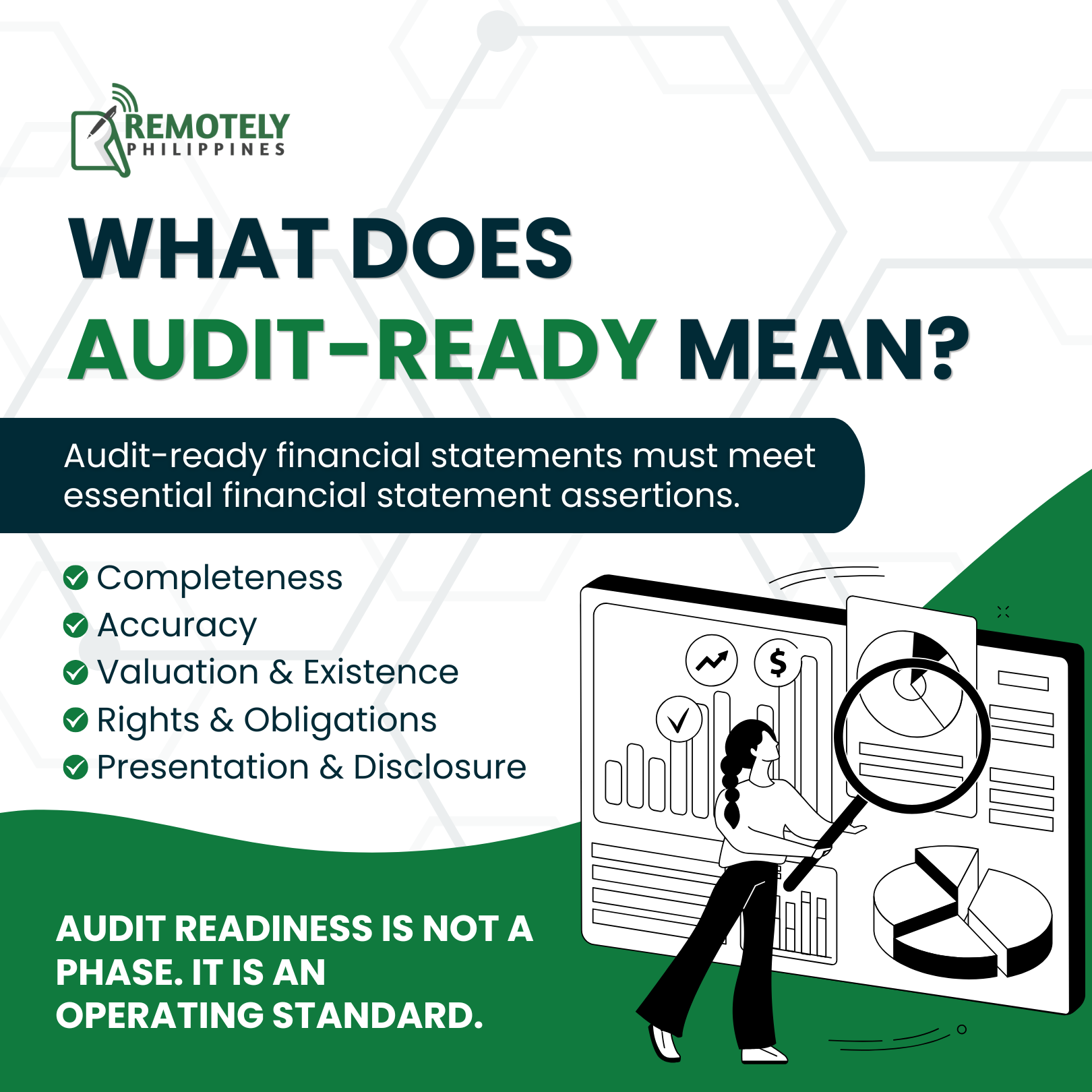

What “Audit-Ready” Means Beyond Accuracy

A common misconception among finance teams is that audit readiness is achieved once the trial balance is finalized and internally reviewed. In reality, this is only the starting point. Audit-ready financial statements must satisfy the relevant financial statement assertions, including

completeness, accuracy, valuation, existence, rights and obligations, and presentation and disclosure.

These are not abstract principles; they form the basis of how auditors evaluate whether financial information is fairly stated. For practical purposes, audit readiness requires that financial data is complete, properly valued, and fully supported by sufficient and appropriate audit evidence. These core elements operationalize the broader set of assertions and ensure that balances can withstand audit scrutiny.

Maintaining audit readiness requires ensuring that financial data satisfies the relevant financial statement assertions and is supported by sufficient and appropriate audit evidence at all times, not just during audit season. This reinforces a key audit principle:

financial statements must be continuously supportable, not retroactively justified.

In practical terms, this means every material balance should be traceable to underlying documentation, whether that is a contract, invoice, bank confirmation, or system-generated report. When that traceability is missing, audit risk increases immediately.

Where Audit Readiness Is Built: Inside the Close and Reconciliation Process

From an audit practitioner’s perspective, the financial close is the foundation of audit readiness. A

structured year-end close, supported by reconciled accounts and reviewed schedules, is critical to minimizing audit adjustments. However, the deeper issue is not year-end execution; it is whether those disciplines exist throughout the year.

Organizations that rely on year-end clean-up often face compounded issues. Reconciliations become more complex, variances are harder to explain, and supporting documentation may no longer be readily available. Failure to perform regular account reconciliations is a leading contributor to audit delays.

This is consistent with audit experience, where unresolved reconciling items often trigger expanded testing and additional documentation requests. In contrast, companies that perform monthly reconciliations and variance analysis effectively distribute audit work across the year. The implication is straightforward. A disciplined close process does not just improve reporting accuracy. It directly reduces audit risk and effort.

Documentation: The Most Underrated Driver of Audit Outcomes

If there is one consistent theme across audit engagements, it is this: documentation quality determines audit efficiency.

Organizations that maintain organized and

accessible financial records year-round are significantly better positioned to respond to audit requests without disruption.

Internal Controls and Their Direct Impact on Audit Scope

Audit readiness cannot be separated from internal controls over financial reporting. Auditors assess not only whether financial statements are reasonable, but whether the processes producing those statements are reliable. When controls are well-designed and consistently executed, auditors can place reliance on them. This reduces the extent of substantive testing required.

Establishing and maintaining strong internal controls as part of audit preparation. This includes clear approval processes, segregation of duties, and documented review procedures. Where these controls are weak or inconsistently applied,

auditors compensate by increasing testing. This has a direct impact on audit timelines and effort. From a finance leadership perspective, this creates a clear linkage: stronger controls lead to more efficient audits and fewer findings.

Accounting Estimates: Where Audits Become Most Technical

Among all areas of financial reporting,

accounting estimates consistently receive the highest level of audit scrutiny.

Estimates inherently involve judgment, whether in revenue recognition, provisions, or asset valuations. What distinguishes audit-ready organizations is not the absence of judgment, but the quality of support behind it.

This heightened scrutiny is driven by the inherent risk characteristics of estimates. Unlike transactional accounts, estimates are not directly observable and often rely on management assumptions, forward-looking information, and internal models.

It introduces estimation uncertainty, increases susceptibility to bias, and limits the availability of objective corroborating evidence.

As a result, auditors place greater focus on evaluating the reasonableness of assumptions, the consistency of methodologies, and the reliability of underlying data. While the sources emphasize documentation broadly, audit practice reinforces that estimates must be supported by reasonable assumptions, consistent methodologies, and clear documentation of changes over time.

Without this, auditors are required to perform additional procedures, often involving independent recalculations or third-party data. This is one of the most common areas where audits slow down, not because estimates are incorrect, but because they are insufficiently supported.

Technology and the Shift Toward Continuous Audit Readiness

The concept of “staying audit-ready all year” is strongly emphasized by many, particularly as organizations adopt more digital and automated financial processes. Technology plays a critical role in sustaining audit readiness. Automated systems reduce manual errors, enforce consistency, and maintain audit trails that are easier to review and validate.

More advanced environments are moving toward continuous monitoring, where anomalies are identified closer to real time. This shift has practical implications. It reduces the need for large-scale corrections at year-end and supports a more stable, predictable audit process.

For growing organizations, this is becoming less of an advantage and more of a necessity.

Operational Support in Sustaining Audit Readiness

Even well-structured finance teams encounter a practical constraint: capacity. Audit readiness requires consistency across multiple layers, reconciliations, documentation, controls, and review. While these are straightforward in principle, they are execution-heavy in practice. During peak periods, especially around month-end and year-end, teams are often forced to prioritize deadlines over process discipline.

This is where gaps begin to form. Incomplete reconciliations, delayed documentation, and rushed reviews are rarely due to a lack of expertise. More often, they reflect bandwidth limitations. Over time, these small gaps accumulate and surface during audit fieldwork as delays, follow-ups, and adjustments. Organizations that sustain audit readiness typically address this not by overextending internal teams, but by reinforcing them.

Thus, organizations that leverage a remote

operational support team are able to maintain control without compromising efficiency. Routine but critical processes, such as account reconciliations, audit schedule preparation, and documentation management, can be executed with consistency, ensuring that internal teams remain focused on higher-value analysis and decision-making.

In this model, support functions as an extension of the finance team, not a replacement. It strengthens execution where it matters most, at the process level, where audit readiness is either built or lost.

FAQs

Conclusion: Audit Readiness as an Operating Standard

From a CPA and audit practitioner standpoint, the most effective organizations do not treat audit readiness as a phase. They treat it as a standard. The consistent message of this article is clear: audit readiness is achieved through

consistency, structure, and continuous discipline, not last-minute preparation.

Finance leaders who embed these principles into their operations do more than improve audit outcomes. They strengthen financial governance, enhance reporting reliability, and position their organizations for scalable growth. Ultimately, audit readiness is not about passing an audit. It is about being able to defend your numbers at any time, without hesitation.